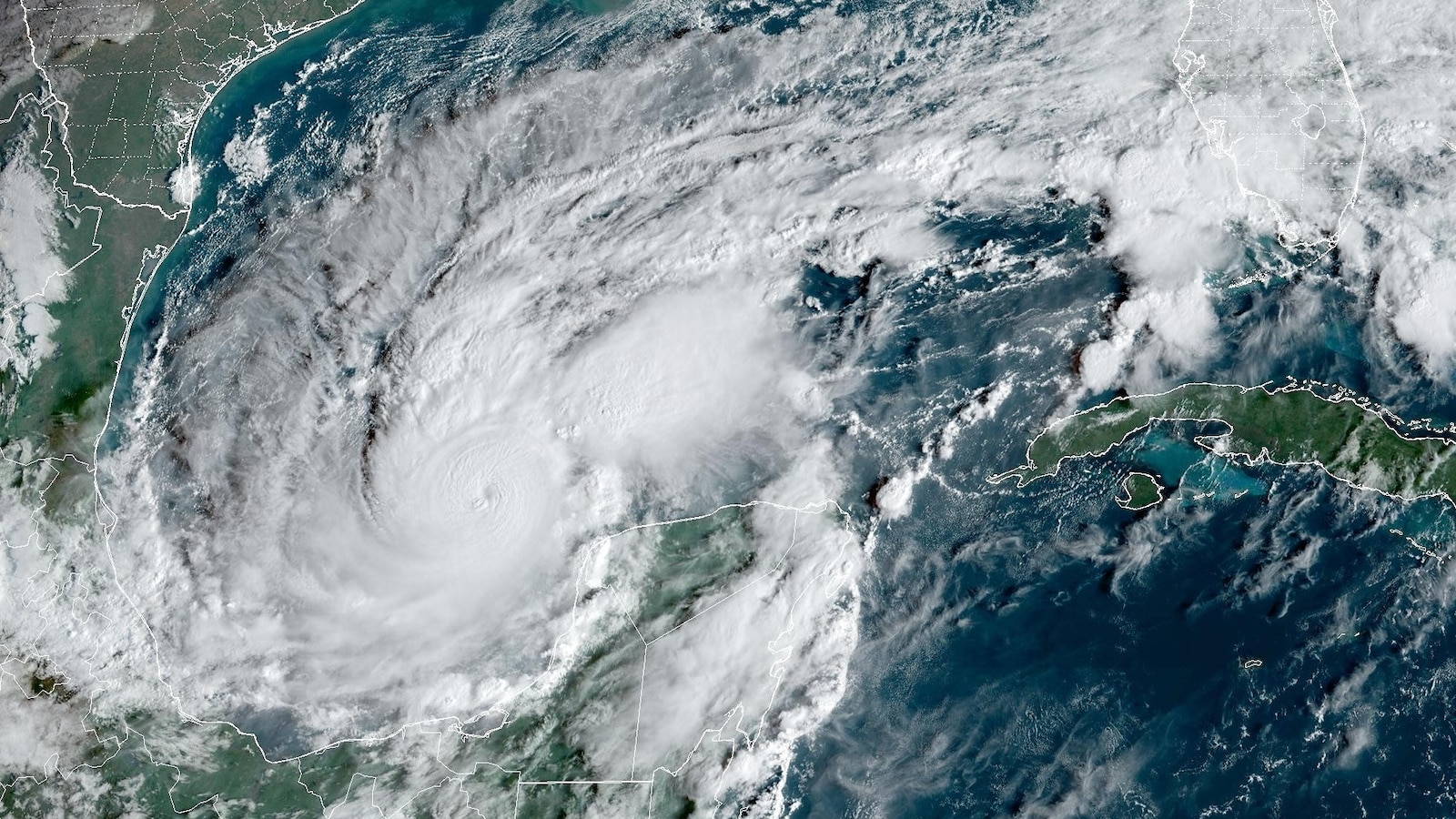

Milton rapidly intensified to a Category 5 hurricane late Monday morning.

Within hours, Milton strengthened to a Category 2, then a Category 3, then a Category 4 and finally a Category 5.

Milton now ranks as the third-greatest 24-hour wind speed intensification for a hurricane in the Atlantic Basin. (Records are based on data since the satellite era began in the 1960s.)

At least the insurance companies will only have to rebuild some houses once after 2 hurricanes

If your policy covers wind they claim the damage is from water. If your policy covers water, they claim the damage is from wind. If your policy covers both, they claim a hurricane is exempt as an act of god.

I want to bitch about insurance companies but insurance is for something that is unavoidable.

All this shit is becoming more and more avoidable.

Which, to be fair, is really about all they can do. You CANNOT stop a hurricane from obliterating a house. There is NOTHING the average American can do about it except leave and hope it survives.

Then its dishonest to accept money for your fake business.

they are not real businesses in the insurance sense. its all federal money for flood insurance. they’re just servicers kinda like mortgage originators.

That sounds like capitalistic socialism to me. I dont even understand the notion of what you said there.

this goes into it a bit and is a good listen in general. https://overcast.fm/+AAyIOzvst0E

Insurance companies don’t build shit. They just collect money from people, and sometimes give some of it back.

They’re actually required to give 85% of everything back, so they give back most of it. It seems like Florida is becoming too much of a hassle to insure, though. Some companies have pulled out of florida.

Everyone in FL should have pulled out.

This joke works on multiple levels and I’m happy about that.

Holy shit a triple entendre!

https://www.youtube.com/watch?v=d8GR0KDYtNQ

Does that 85% include their costs or is that the full amount returned to policy holders?

Full amount that is legally required to pay back out in insurer coverage every year. The other 15% covers pay roll, rent, buildings, bonus’, overhead, etc. Literally everything else. Same deal for medical insurance.

Begrudgingly cover*

unless they can find a way to screw you over for profit, then they absolutely will no matter how ridiculous the “reasoning”*

I believe it was Katrina where the insurance said it was wind damage when you only had flood insurance, but if you’re neighbor only had wind coverage they’d tell them it was water damage.

Right storm. Wrong details.

They (insurance companies) were claiming it as flood/surge damage, even if wind ripped off your roof to let the water inside. Wind was covered, water wasn’t. Companies were sued for trying to blanket deny an area based on one generic engineering report, or denying coverage if flood waters came through after wind destroyed a place. Insurance com0anies don’t typically offer flood insurance to a lot of places and if homeowners want it, they have to buy it through the federal government.

Many insurance companies won’t even insure homes in much of Florida.

And the rest are probably planning to.

What insurance companies? They all backed out of Florida years ago. Now it’s state funded home insurance footing the bill.

I read a thing recently that insurance companies are getting increasingly skittish all over the country, even places that wouldn’t traditionally be considered risky, because yay, climate change.

The interesting thing about it was that insurance companies’ insurance is increasingly the thing that’s causing issues, because it’s getting harder for the risk to be spread out. That is to say that insurance companies financially rely on areas with low rates of natural disasters because they end up being a net positive due to insurance premiums and no need for payout. Fewer of these “safe” areas mean the insurance companies struggle to stay solvent and have to rely on their own insurance policies to have their back, but those meta-insurance companies have apparently been historically loud about climate change — probably because besides the government, they’re the ones who have to pony up

Here in Missouri, home owners insurance is starting to lose hail damage from coverage. Damn near 90% of the houses around my area have now replaced their roofs, and have the roofing signage out front. It’s almost a running joke now: guessing which house will be next to get one, and counting the company’s signs to see who’s making a killing.

No problem. The 0ld coots in Florida that vote won’t be around when the bill comes due.

If people don’t have the common sense to not build houses in places that are guaranteed to be destroyed by a natural disaster sooner than later, then I shouldn’t have to subsidize their rebuilding costs through my insurance premiums.

That’s what the people in the North Carolina mountains thought.

That seems like a perfectly reasonable place to build that’s not obviously at threat from hurricanes. But sometimes shit happens that couldn’t be easily foreseen, and THAT’S what insurance is for.

My point, however, is that insurance is NOT to make other policy holders foot the expense of someone repeatedly repairing/rebuilding after completely foreseeable/inevitable events.

To anyone that insists on having a house right on the beach on the Gulf Coast, I say, “Insure thy self.”

Yeah, used to be that insurance costs were almost directly skewed based on risk. But then people were upset that it costed so much to insure some places(the ones that should be prohibitively expensive to insure). And then slowly over time they baked in little increases in price everywhere else to subsidise huge price cuts in those areas to out-compete the companies that put the onus entirely on the people taking risks. Eventually, as it became more and more widespread to do that, it became financially more viable to spread it out rather than have drastically more expensive areas. And now we all have to partially cover people who are taking way more risk than we would.

That’s communism in a nut shell, Republicans should be up in arms over it

Forms of communism that mean they are making more money are actually ok by them. They just have to find a different name to call it so they don’t have to say that icky word that gives them feelings.

That or build something that can stand up to being hit. Tall order, but the inner armchair engineer in me thinks it’s like, totally possible.

I think you forget, building it stronger once would cost 50% more upfront. Better to build it twice, or three times at only 100% cost each time. That way you can be the lowest bidder every time.